Canada’s household saving rate sat at approximately 4.4% of disposable income as of Q4 2025, down from 5.2% the quarter prior, according to Statistics Canada. Choosing the right budgeting system can meaningfully move that needle for individual households.

QUICK STAT

Real-World Example: The Sharma Family in Mississauga

Let’s make this tangible. Take the Sharma family: two working adults in Mississauga, combined take-home pay of $8,800/month (or $4,400 per bi-weekly paycheque each, combined).

Under a monthly budget, they allocate their $8,800 to fixed and variable expenses and save whatever is left at month’s end — which, after life gets in the way, is often $200-$400.

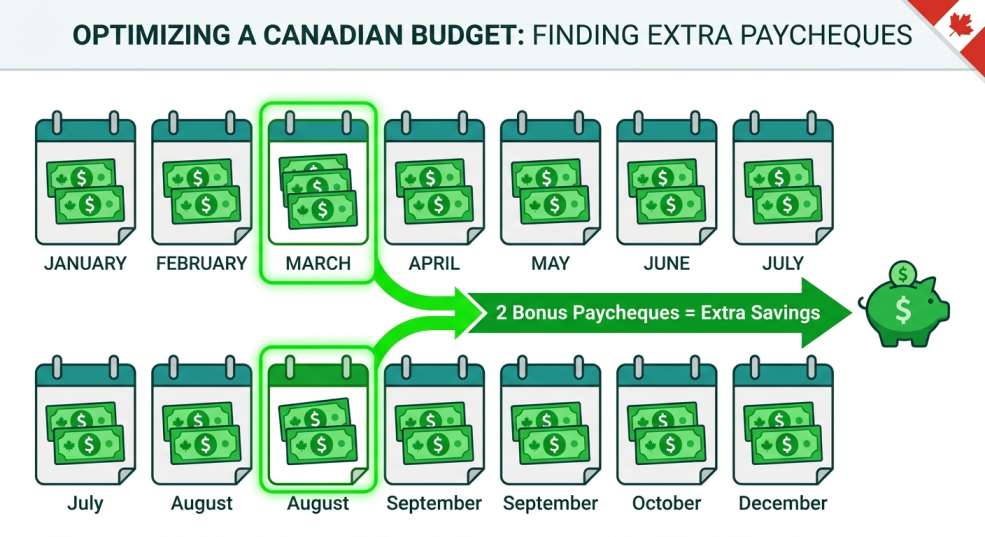

Under a bi-weekly budget, each $4,400 combined paycheque has a specific plan. In the two ‘three-paycheque months’ of the year, that third $4,400 paycheque — which isn’t needed for any regular bills — goes entirely into savings. That’s $8,800 extra saved per year, just from being intentional about paycheque timing.

TABLE 1: Bi-Weekly vs. Monthly Budgeting — Head-to-Head Comparison

Feature | Bi-Weekly Budgeting | Monthly Budgeting |

Pay cycle alignment |

|

|

Number of budget cycles/year | 26 | 12 |

‘Bonus’ paycheque strategy |

|

|

Overspending detection |

|

|

Setup complexity |

|

|

Best for debt repayment |

|

|

Works with irregular income |

|

|

TFSA/RRSP automation ease |

|

|

Cash flow visibility |

|

|

Recommended for | Salaried bi-weekly employees | Self-employed, monthly earners |

Perfect match for 43% of Canadians

Perfect match for 43% of Canadians Requires manual conversion

Requires manual conversion Easy to overlook

Easy to overlookThe Real Savings Math: What the Numbers Actually Show

Scenario 1: The Bi-Weekly Advantage on Debt Repayment

One of the most dramatic demonstrations of bi-weekly power is mortgage repayment. This principle extends to any installment debt.

Consider a $450,000 mortgage in Ontario at 4.5% interest amortized over 25 years. With monthly payments, you make 12 payments per year. Switch to accelerated bi-weekly payments (half the monthly amount paid every two weeks), and you effectively make 13 full payments per year — because 26 half-payments equals 13 full payments, not 12.

The result? That mortgage is paid off approximately 3 years and 2 months faster, saving tens of thousands in interest. While this is specifically about mortgage payment frequency (not budgeting frequency), the same mathematical principle applies to how you structure and prioritize debt payments within a bi-weekly budget.

Source: The mechanics of accelerated bi-weekly mortgage payments are well-documented by Canadian mortgage professionals and lenders. See LoanCalculator.ca for interactive examples.

Scenario 2: TFSA Contributions — Timing Matters

The 2026 TFSA contribution limit is $7,000 annually ($583/month). Under a monthly budget, many Canadians set up a $583/month auto-transfer — and that works fine. But bi-weekly budgeters can align their $269 bi-weekly contribution exactly with paydays, reducing the risk of the transfer bouncing if the timing is off, and taking advantage of those two extra paycheques to top up faster in bonus months.

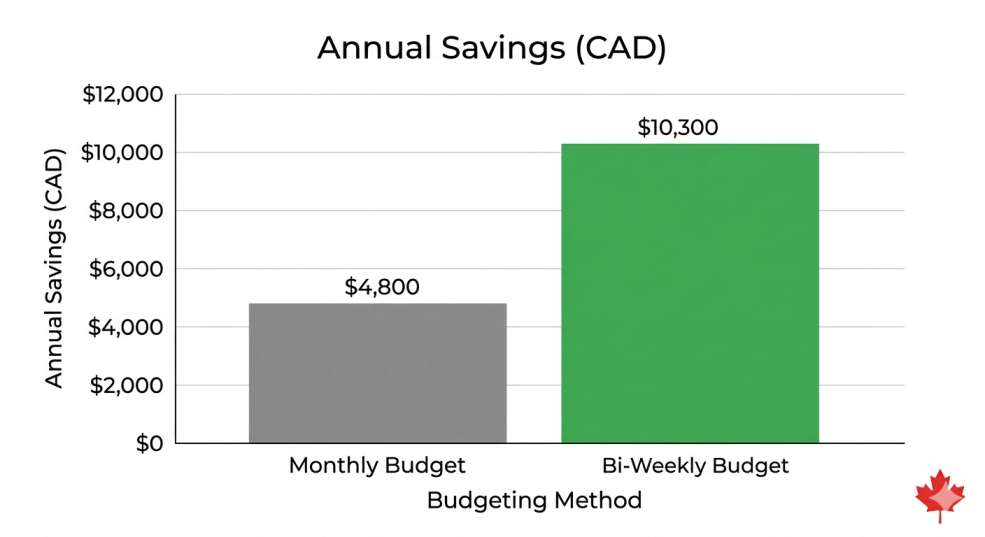

TABLE 2: Annual Savings Potential by Budgeting Method (Sample Canadian Household)

Based on a household with $90,000 combined net annual income:

Savings Category | Monthly Budget (Typical) | Bi-Weekly Budget (Optimized) | Annual Difference |

Regular monthly savings | $4,800/yr ($400/mo) | $4,800/yr (same base) | $0 |

‘Bonus paycheque’ capture | $0 (unplanned) | $4,500/yr (2 extra cheques) | +$4,500 |

Debt interest saved (accel. payments) | Baseline | Est. $600-$1,200/yr less interest | +$600-$1,200 |

Impulse spending reduction* | Baseline | Est. $300-$800 less/yr | +$300-$800 |

TOTAL ESTIMATED ADVANTAGE | — | — | +$5,400-$6,500/yr |

*Impulse spending reduction is estimated based on the documented effect of shorter budget review cycles increasing spending awareness. Individual results will vary.