I’ll never forget the sinking feeling I had when my car broke down on a freezing February morning in Toronto. The repair bill? $847. My emergency savings? $0.

If you’ve ever experienced that gut-wrenching moment when an unexpected expense hits and you’re not prepared, you’re not alone. According to recent data from the Canadian Investment Regulatory Organization, nearly one in three Canadians had to borrow money just to cover daily expenses in the past year. Even more concerning, only 64% of Canadians have enough saved to cover three months of expenses.

Here’s the truth: you don’t need a six-figure salary or years of time to build financial security. You need a solid plan, realistic goals, and strategies that actually work with your current income.

In this comprehensive guide, I’ll walk you through exactly how to save your first $1,000 in just 90 days—even if you’re living paycheque to paycheque right now. This isn’t about extreme couponing or eating ramen for three months. It’s about smart, sustainable changes that create lasting financial stability.

Why $1,000 is the perfect starter emergency fund target – The exact 90-day timeline to reach your goal – Practical money-saving strategies tailored to Canadian budgets – Where to keep your emergency fund for maximum accessibility and growth – How to maintain and grow your fund after hitting your goal

What you’ll learn.

Let’s turn financial anxiety into financial confidence—starting today.Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Understanding the $1,000 Emergency Fund: Why This Number Matters

The Psychology Behind Starting Small

When financial experts recommend saving three to six months of expenses, most Canadians feel overwhelmed before they even start. If your monthly expenses are $3,000, that’s $9,000 to $18,000—a number that feels impossible when you’re already stretched thin.

The $1,000 emergency fund is different. It’s achievable, yet substantial enough to cover most common unexpected expenses: – Minor car repairs ($500-$800) – Urgent dental work ($300-$700) – Emergency home repairs like a broken water heater ($600-$900) – Last-minute travel for a family emergency ($400-$800) – Pet emergency vet visits ($500-$1,000)

SOURCE: Financial Consumer Agency of Canada data on typical emergency expenses

This “starter emergency fund” serves a critical purpose: it breaks the debt cycle. Without it, these unexpected costs force you onto credit cards, payday loans, or lines of credit—each carrying interest rates that make your financial situation worse, not better.

What the Data Shows About Emergency Savings in Canada

Recent surveys reveal concerning trends about Canadian financial resilience:

[TABLE 1: Canadian Emergency Fund Statistics]

| Statistic | Percentage | Source |

|---|---|---|

| Canadians with 3+ months expenses saved | 64% | CFCS 2019 Survey |

| Canadians who borrowed for daily expenses (past year) | 33% | CIRO Survey 2024 |

| Canadians with less than $1,000 in savings | 31% | MNP Consumer Debt Index |

| Average unexpected expense faced annually | $1,200-$1,800 | Financial literacy studies |

SOURCE: Canadian Financial Capability Survey 2019, CIRO Survey 2024, MNP Consumer Debt Index

The gap between where Canadians are and where they need to be is significant—but not insurmountable. The key is starting with a realistic, achievable goal.

The 90-Day Emergency Fund Blueprint: Your Complete Action Plan

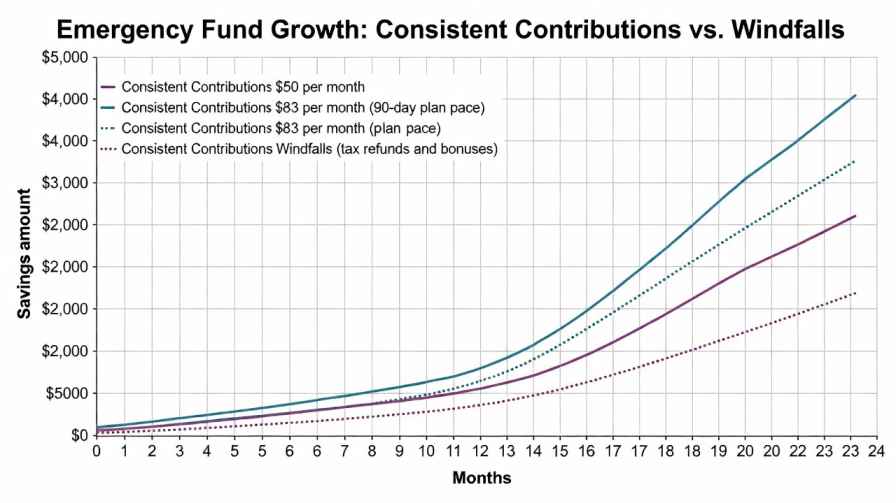

Month 1 (Days 1-30): Foundation & Quick Wins – Target: $333

The first month is about momentum. You’re building the habit of saving while implementing strategies that produce immediate results.

Week 1: Audit & Activate (Days 1-7)

Day 1-2: Complete Financial Inventory – Calculate your true monthly expenses (use Canada.ca Budget Planner) – Identify your exact take-home income – List all subscriptions and recurring charges – Document where every dollar currently goes

Day 3-4: Open Your Dedicated Emergency Fund Account Choose a high-interest savings account (HISA) or TFSA with these features: – No monthly fees – No minimum balance requirements – Competitive interest rate (3-5% currently available in Canada) – Easy online access but not linked to daily spending accounts

Top Canadian options include: – EQ Bank Savings Plus Account (no fees, competitive rates) – Tangerine Savings Account (welcome bonus rates) – Simplii Financial High Interest Savings Account – Wealthsimple Cash (TFSA option available)

SOURCE CITATION NEEDED: Current HISA rates from ratehub.ca or financial comparison sites

Day 5-7: Execute the Low-Hanging Fruit – Cancel unused subscriptions (average savings: $50-$100/month) – Call service providers (internet, phone, insurance) to negotiate better rates (average savings: $30-$80/month) – Switch to no-fee banking if you’re paying monthly account fees

Expected Week 1 Savings: $80-$180

Week 2-4: Implement Core Saving Strategies

The Bi-Weekly Savings Schedule

Instead of monthly goals, break your target into smaller, more manageable chunks:

[TABLE 2: 90-Day Savings Breakdown]

| Period | Days | Savings Target | Weekly Goal | Strategy Focus |

|---|---|---|---|---|

| Month 1 | 1-30 | $333 | $83 | Quick wins, habit building |

| Month 2 | 31-60 | $333 | $83 | Income boosting, expense cutting |

| Month 3 | 61-90 | $334 | $83 | Maintenance, final push |

| Total | 90 | $1,000 | $83 avg | Complete foundation |

This breakdown makes the goal feel achievable. Saving $83 per week is manageable; saving $1,000 feels overwhelming.

Month 2 (Days 31-60): Acceleration & Income Boosting – Target: $333

By month two, you’ve built momentum. Now it’s time to accelerate growth through a two-pronged approach: deeper expense cuts and modest income increases.

Expense Optimization Strategies

1. The “Needs vs. Wants” Audit Review every expense through this lens: – Need: Essential for survival, health, or work – Want: Enhances quality of life but not essential

Canadian-specific areas where most people find savings: – Groceries: Switching to No Frills or FreshCo instead of premium stores (savings: $100-$200/month) – Coffee/takeout: Making coffee at home 4 days/week (savings: $60-$80/month) – Transportation: Carpooling, taking transit once weekly, or combining errands (savings: $40-$100/month) – Entertainment: Using free community resources, libraries, outdoor activities (savings: $50-$100/month)

2. The Reverse Budget Method Traditional budgeting feels restrictive. Try this instead: – Set your savings goal first ($83/week = $332/month) – Transfer that amount immediately when paid – Live on what’s left

This “pay yourself first” approach ensures savings happen automatically.

Modest Income Boosting (Canadian Context)

You don’t need a full side hustle. Small income additions make a big difference:

Low-Effort Options: – Survey sites: Swagbucks, Survey Junkie (extra $50-$100/month) – Cashback apps: Rakuten, Drop for regular purchases (extra $20-$40/month) – Selling unused items: Kijiji, Facebook Marketplace (one-time boost of $100-$300) – Freelance your skills: Fiverr Canada, Upwork for a few hours monthly (extra $100-$300/month)

Medium-Effort Options: – Food delivery: Skip the Dishes, Uber Eats on weekends (extra $200-$400/month) – Pet sitting: Rover Canada during busy seasons (extra $150-$300/month) – Tutoring: If you have expertise, online tutoring pays $25-$50/hour – Seasonal work: Tax season prep at H&R Block, retail during holidays (extra $300-$600/month)

Sarah from Calgary combined selling old furniture ($240), doing three food delivery shifts monthly ($180), and using cashback apps ($30) to add an extra $450 to her emergency fund in Month 2 alone.

Real Example

Month 3 (Days 61-90): Final Push & Habit Solidification – Target: $334

You’re in the home stretch. Month three is about maintaining momentum and ensuring these habits stick beyond the 90-day period.

The Windfall Strategy

During your 90-day journey, watch for these potential windfalls: – Tax refunds: If you receive one, allocate 50-100% to your emergency fund – GST/HST credits: Quarterly payments from the CRA for eligible Canadians – Work bonuses: Any unexpected employment income – Birthday/holiday money: Adult gift money often goes unallocated – Bottle returns: In provinces with deposit systems, collecting returns adds up

Pro tip: Set up CRA direct deposit to ensure tax refunds and credits go straight to your emergency fund account.

Challenge Yourself with Money-Saving Experiments

Make the final month engaging with these challenges:

No-Spend Weekends: Choose 2-3 weekends where you spend nothing beyond essentials. Find free activities like hiking, library visits, or game nights at home.

The $5 Rule: Every time you receive a $5 bill in change, save it immediately. This mindless saving technique adds up quickly.

The 30-Day Rule: For any non-essential purchase over $50, wait 30 days. If you still want it, consider it. Often, you’ll forget about it.

Strategic Account Selection: Where to Keep Your Emergency Fund in Canada

Choosing the right account for your emergency fund requires balancing three priorities: accessibility, growth, and protection.

High-Interest Savings Accounts (HISAs)

Best for: Most people building their first emergency fund

Advantages: – Immediate access to funds (1-2 business days) – CDIC insured up to $100,000 – No withdrawal penalties – Competitive interest rates (3-5% as of early 2025)

Considerations: – Interest is taxable in non-registered accounts – Rates can fluctuate with Bank of Canada policy changes

SOURCE: Current CDIC insurance limits and HISA rate ranges

Tax-Free Savings Accounts (TFSAs)

Best for: Those with available TFSA contribution room

Advantages: – Tax-free growth and withdrawals – Can hold cash, GICs, or investments inside – Contribution room is reinstated after withdrawals – Current limit: $7,000 for 2025

Considerations: – Must track contribution room carefully – Overcontributions face 1% monthly penalty – Withdrawn amounts can only be re-contributed the following year

SOURCE: CRA current TFSA contribution limits

[TABLE 3: Emergency Fund Account Comparison]

| Account Type | Interest Rate Range | Tax Status | Accessibility | Best For |

|---|---|---|---|---|

| Regular HISA | 0.5-2.5% | Taxable | Immediate | Quick access needs |

| Premium HISA | 3-5% | Taxable | 1-2 days | Balance seekers |

| TFSA (Cash) | 3-5% | Tax-free | 1-2 days | Maximum growth |

| TFSA (GIC) | 4-6% | Tax-free | Locked-term | Partial emergency funds |

What to Avoid

RRSPs: Withdrawals are taxed as income and permanently lose contribution room (except for HBP/LLP programs)

Investment accounts: Emergency funds need stability, not market volatility

Chequing accounts: Too accessible leads to accidental spending; minimal or no interest

Common Obstacles & How to Overcome Them

“My Budget Is Already Maxed Out”

This is the most common objection—and the most surmountable. Here’s what worked for real Canadians:

Maria’s Story (Vancouver): “I thought there was no room in my budget. Then I tracked every purchase for two weeks. I was spending $180/month on ‘small’ purchases—coffee, convenience store snacks, impulse Amazon buys. I didn’t even realize it. Cutting just half of those freed up $90/month.”

Action Steps: – Track spending for 14 days using an app (Mint, YNAB, or even a notes app) – Identify your personal “money leaks” – Eliminate or reduce just the top 2-3 wasteful categories

“An Emergency Always Comes Up”

This creates a frustrating cycle where you can never build savings. The solution is implementing a two-tier system:

Tier 1: Immediate Emergency Fund ($250-$500) Keep this ultra-accessible for true emergencies that can’t wait.

Tier 2: Building Fund This is your $1,000 goal. It’s accessible but requires slightly more effort to withdraw (different bank, no debit card attached).

Psychological trick: The small barrier of transferring money first gives you time to evaluate if it’s truly an emergency.

“I’m Dealing With Debt”

The debt vs. savings dilemma is real. Here’s the balanced approach:

If you have high-interest debt (19%+ credit cards): – Save your first $500 for emergency fund – Then aggressively pay down high-interest debt – Once debt is manageable, complete your $1,000 fund

If you have medium-interest debt (6-12% personal loans): – Split efforts: 50% to emergency fund, 50% to debt – Having some emergency savings prevents adding more debt

If you have low-interest debt (4-6% car loans, student loans): – Prioritize building full emergency fund first – These debts are manageable and less urgent

Advanced Strategies: Accelerating Beyond 90 Days

Once you hit your $1,000 goal (congratulations!), don’t stop. Here’s how to keep building financial resilience:

The Ladder Approach to Long-Term Emergency Funds

Step 1: Starter Fund ($1,000) ✓ You’re here! Step 2: Enhanced Protection ($2,500) Step 3: One-Month Coverage (your monthly expenses) Step 4: Three-Month Security (3x monthly expenses) Step 5: Six-Month Stability (6x monthly expenses)

Work through these steps at your own pace. Even an extra $50/month gets you to Step 2 in just 30 months.

Setting Up Automatic Growth

Once your foundation is solid: 1. Set up automatic bi-weekly transfers ($25-$50) 2. Allocate 25-50% of future raises to emergency savings 3. Use tax refunds to jump levels quickly 4. Review and increase contributions annually

The Interest Optimization Strategy

As your emergency fund grows beyond $2,000, consider splitting it: – 70% in HISA: Immediate access, guaranteed safety – 30% in 1-year GICs: Higher interest, acceptable wait time for non-urgent access

This strategy maximizes returns while maintaining adequate liquidity.

Canadian-Specific Considerations & Resources

Government Programs & Credits That Can Help

GST/HST Credit – Quarterly payments for low-to-moderate income Canadians – Up to $519 annually for singles, more for families – Strategy: Set up direct deposit to your emergency fund account

Canada Workers Benefit (CWB) – Refundable tax credit for low-income workers – Up to $1,428 for singles (2024) – Includes advance payments option

Provincial Programs Each province offers additional supports: – Ontario: Trillium Benefit – BC: Climate Action Tax Credit – Quebec: Solidarity Tax Credit – Alberta: Various family supports

SOURCE: Current CRA benefit amounts and provincial program details

Free Financial Resources for Canadians

Credit Counselling Societies Non-profit organizations offering free advice: – Credit Counselling Society (BC, Alberta) – Ontario Credit Counselling Services – Fédération des associations coopératives d’économie familiale (Quebec)

Financial Consumer Agency of Canada (FCAC) – Free budget planner tools – Emergency fund calculator – Financial literacy resources

Public Libraries Free access to: – Financial literacy workshops – One-on-one financial coaching (some locations) – Books and resources on personal finance

Maintaining Your Emergency Fund: Long-Term Success Strategies

When (and When Not) to Use Your Emergency Fund

True Emergencies: ✓ Unexpected medical or dental expenses ✓ Essential car repairs to get to work ✓ Job loss or sudden income reduction ✓ Urgent home repairs (broken furnace, leaking roof) ✓ Emergency family travel

Not Emergencies: ✗ Holiday shopping ✗ Regular maintenance (winter tires, oil changes) ✗ Vacations or “deals too good to pass up” ✗ Planned expenses you forgot to budget for ✗ Discretionary purchases

The 48-Hour Rule: Before using emergency funds, wait 48 hours if possible. This cooling-off period helps distinguish true emergencies from impulse decisions.

Replenishing After Use

If you need to tap your emergency fund: 1. Don’t feel guilty—that’s what it’s for 2. Pause long-term savings goals temporarily 3. Redirect that money to rebuilding your emergency fund 4. Aim to replenish within 3-6 months 5. Resume normal savings once restored

Annual Review & Adjustment

Set a yearly “Emergency Fund Check-up” date: – Review if $1,000 is still adequate (life changes, expenses increase) – Assess your account choice (are rates still competitive?) – Evaluate if you’re ready to move to the next tier – Update beneficiaries if held in TFSA

Real Canadian Success Stories

James, 34, Edmonton

Starting point: $0 in savings, $35,000 salary 90-day result: $1,240 saved

“I used the reverse budget method—paid myself first every payday. The biggest game-changer was getting a second job delivering food two Saturdays per month. That alone contributed $400 of my savings. The rest came from cutting my expensive phone plan and eating out less.”

Priya, 28, Toronto

Starting point: $200 in savings, $45,000 salary, $8,000 credit card debt 90-day result: $1,080 saved while paying minimum debt payments

“I focused on the $1,000 emergency fund first, even though I had debt. Three weeks in, my laptop died. Instead of adding $600 to my credit card, I could pay cash from my emergency fund. I’m rebuilding it now, but that one moment proved why this matters.”

Robert & Michelle, 41 & 39, Winnipeg

Starting point: $500 in savings, $82,000 combined income, two kids 90-day result: $1,400 saved

“As a family, cutting expenses felt impossible. Then we realized we were spending $380/month on subscription services, meal kits, and memberships we rarely used. Cutting half of those freed up $190/month. Add in a tax refund we got in Month 2, and we exceeded our goal.”

Your 90-Day Checklist: Quick Reference Guide

Week 1

□ Calculate total monthly expenses □ Open dedicated emergency fund account □ Cancel unused subscriptions □ Make first deposit ($80+)

Week 2-4

□ Set up automatic transfers □ Implement expense tracking system

□ Execute first cost-cutting measures □ Reach Month 1 goal ($333)

Week 5-8

□ Review and optimize recurring expenses □ Start modest income-boosting activity □ Apply windfalls to emergency fund □ Reach Month 2 goal ($666 total)

Week 9-12

□ Maintain all established habits □ Celebrate milestones along the way □ Plan for post-90-day continuation □ Reach $1,000 goal

Conclusion: Your Financial Safety Net Starts Today

Building a $1,000 emergency fund in 90 days isn’t about deprivation or massive lifestyle changes. It’s about intentional small actions that compound over time.

The key principles we’ve covered:

Start with clarity: You need to know where your money goes before you can redirect it. The financial audit isn’t optional—it’s foundational.

Embrace automation: Willpower fails. Systems succeed. Automatic transfers remove the decision fatigue that kills savings plans.

Progress over perfection: Saving $75 in a week when you planned for $83 is still progress. Don’t abandon the plan because you fell short.

Celebrate milestones: Hit $250? Take a moment to acknowledge it. Hit $500? That’s worth celebrating. Small wins maintain motivation for the long haul.

Think beyond 90 days: This isn’t just about $1,000. It’s about building financial resilience that protects you for life.

The difference between financial stress and financial peace isn’t usually a dramatic income increase—it’s having a cushion between you and life’s inevitable surprises. That cushion starts with $1,000 and your decision to start building it today.

Your next step is simple: Open that emergency fund account this week. Make the first deposit, even if it’s just $20. The journey from $0 to $1,000 starts with a single transfer.

Ninety days from now, you’ll thank yourself for starting today.