If you’re staring down $20,000 in debt — whether it’s credit card balances, a personal loan, a line of credit, or some combination of all three — the idea of clearing it in 12 months might sound like a fantasy. But for average-income Canadians willing to get serious and follow a proven system, it’s more achievable than you think.

Here’s the hard truth: Canadians carry some of the highest household debt loads in the developed world. According to Statistics Canada, the ratio of household credit market debt to disposable income stood at 173% in late 2024 — meaning for every $1 of income, Canadians owe $1.73 in debt. [Source: Statistics Canada, National Balance Sheet and Financial Flow Accounts, Q3 2024 ]

And credit card debt is accelerating. The average Canadian credit card balance hit $4,562 in Q3 2024, up nearly 7% year-over-year. [Source: TransUnion via MoneySense ]

But here’s what the statistics don’t show: thousands of Canadians break free from debt every single year — not because they earned more money, but because they changed their approach. This guide is going to show you exactly how to do it.

In this article, you’ll learn a step-by-step debt repayment plan built specifically for the Canadian context — covering the math, the mindset, the methods, and the money moves that actually work.

Is Paying Off $20,000 in 12 Months Realistic on a Canadian Income?

Let’s do the math before anything else, because clarity beats optimism every time.

To pay off $20,000 in 12 months (not counting interest), you need to put $1,667 toward debt every single month. That’s before interest. If you’re carrying a credit card at 19.99% APR or a personal loan at 12–15%, you’ll need to pay slightly more to account for accumulating interest charges.

Quick math for a $20,000 debt at 19.99% credit card interest:

- Monthly payment needed: ~$1,850–$1,900

- Total interest paid over 12 months at this rate: ~$2,000–$2,200

- Without a plan, minimum payments would take 30+ years and cost over $30,000 in interest

According to Statistics Canada, the median after-tax income for a Canadian individual was approximately $37,899 in recent years — roughly $3,158/month. That means dedicating ~$1,850/month to debt would represent about 59% of take-home pay. Tight, but not impossible — especially if you have a partner contributing or can temporarily boost income.

For a dual-income household at median wages, or a single person earning above median, this is very achievable with disciplined budgeting. The key is treating it as a 12-month sprint, not a lifestyle.

Your Step-by-Step Debt Repayment Plan for Canada

Step 1: List Every Debt You Owe (The Debt Inventory)

You cannot fight what you can’t see. Start by writing out every debt you carry:

- Creditor name

- Balance owing

- Interest rate (APR)

- Minimum monthly payment

- Type of debt (credit card, LOC, personal loan, BNPL, etc.)

Yes, this step is uncomfortable. Many Canadians avoid looking at the full picture because it’s stressful. But this single act of transparency is the foundation of every successful debt repayment plan in Canada.

Step 2: Build a Ruthless But Livable Budget

The goal here isn’t to suffer — it’s to find every available dollar to throw at your debt. Use the 50/30/20 rule as a starting baseline, then adjust aggressively for your 12-month sprint:

- 50% Needs: Rent/mortgage, groceries, utilities, transportation, minimum debt payments

- 30% Wants: Temporarily slashed — eating out, subscriptions, entertainment

- 20% Debt Repayment: In your case, this needs to be more like 50–60% for 12 months

Practical budget cuts for Canadians that actually add up:

- Cancel streaming services you rarely use — $15–$50/month back

- Meal prep and stop buying lunch at work — $200–$400/month back

- Pause gym membership, use free outdoor workouts — $40–$80/month back

- Shop at No Frills, FoodBasics, or Costco instead of Loblaws — $100–$300/month back

- Pause RRSP/TFSA contributions temporarily (controversial, but sensible at high interest rates) — $100–$500/month back

- Downgrade your phone plan — $30–$60/month back

- Cut back on Tim Hortons/Starbucks runs — $50–$150/month back

Canadians often have a ‘subscriptions problem.’ Audit your credit card and bank statements for the past 3 months and highlight every recurring charge. Many people find $100–$300/month in forgotten subscriptions, forgotten free trials, or duplicate services they no longer use.

💡 PRO TIP

Step 3: Choose Your Debt Repayment Strategy

There are two main evidence-backed methods for paying off multiple debts. Here’s how they compare for a debt repayment plan in Canada:

TABLE 1: Debt Snowball vs. Debt Avalanche — Which Is Right for You?

Feature | Debt Snowball | Debt Avalanche |

How it works | Pay minimums on all debts; throw extra at the SMALLEST balance first | Pay minimums on all debts; throw extra at the HIGHEST INTEREST RATE first |

Best for | People who need motivation and quick wins | People who are mathematically focused and disciplined |

Total interest paid | Typically higher | Typically lower (saves more money) |

Time to debt freedom | May take slightly longer | Usually faster if rates vary significantly |

Psychological benefit | High — early wins build momentum | Lower early wins, but bigger savings long-term |

Recommended for $20K goal? | Yes — if you have 3+ debts | Yes — if 1–2 debts at high interest rates |

For most Canadians carrying mixed debt (a credit card at 19.99%, a personal loan at 12%, and a line of credit at 8%), a hybrid approach works well: use the avalanche method on paper, but if you have one small balance under $1,000, pay it off first for the psychological win, then avalanche the rest.

Step 4: Increase Your Income (Even Temporarily)

Budget cuts alone may not be enough — especially if your baseline income is at or below median. That’s where a temporary income boost changes everything. Adding even $400–$600/month in extra income can transform a “barely possible” goal into a comfortable one.

Canadian income-boosting strategies that work in 2025:

- Gig economy: DoorDash, Instacart, Uber Eats, Skip the Dishes — flexible hours, $15–$25/hr after expenses

- Sell items you own: Facebook Marketplace, Kijiji — many Canadians find $500–$2,000 in stuff sitting in storage

- Rent a room or parking space: SpareRoom Canada, Kijiji — $400–$800/month for spare rooms in major cities

- Overtime or a part-time job: Many employers in retail, hospitality, and healthcare actively seek part-time workers

- Freelancing your skills: Writing, graphic design, bookkeeping, IT support — Upwork, Fiverr, LinkedIn

- Tax refund: The average Canadian tax refund is around $1,800 — file early and apply the full amount to debt

Step 5: Automate Your Debt Payments

Willpower is a finite resource. The single best hack for staying on track with your debt repayment plan in Canada is automation. Set up automatic payments — ideally the day after your paycheque hits — so the money goes to debt before you have a chance to spend it.

Most Canadian banks (RBC, TD, Scotiabank, BMO, CIBC, and credit unions) allow you to set up automatic bill payments and transfers. Set your minimum payments to auto-pay on every debt, then set a separate automatic transfer of your “extra” payment to your highest-priority debt on payday.

This is the “pay yourself first” principle — except instead of savings, you’re paying down debt first.

Step 6: Negotiate Lower Interest Rates

This step is underused and underrated. Canadian lenders — including credit card companies — will sometimes lower your interest rate if you simply ask. Especially if you have a history of on-time payments.

Call your credit card company or bank and say: “I’ve been a loyal customer and always paid on time. I’m working to pay down my balance aggressively, but the interest rate is making it difficult. Is there anything you can do to temporarily lower my rate?”

It won’t always work, but it often does. A drop from 19.99% to 14.99% on a $10,000 balance saves you ~$500 in interest over a year — that’s real money.

Also consider a balance transfer to a low-interest credit card or a debt consolidation loan. Many Canadian credit unions offer personal loans at 8–12% — far below typical credit card rates. [Check current rates at your local credit union or on RateHub.ca]

Real-World Scenario: How “Sarah” Paid Off $22,000 in 11 Months

Let’s make this concrete with a realistic example.

Sarah, 34, lives in Hamilton, Ontario, works as an administrative coordinator, and takes home $3,400/month after taxes. She had accumulated $22,000 in debt:

- $11,000 on a Visa credit card at 19.99% APR

- $7,000 personal loan at 13% APR

- $4,000 on a line of credit at 8.5% APR

What Sarah did:

- Cut her monthly expenses by $620 (cancelled subscriptions, meal prepped, dropped gym membership, switched to a cheaper phone plan)

- Started delivering for DoorDash 2 evenings per week, adding $500/month

- Sold unused furniture and electronics on Kijiji for $1,100 lump-sum

- Called Visa and got her rate reduced from 19.99% to 15.99%

- Applied her $1,900 tax refund directly to the Visa balance in March

- Used the avalanche method: hammered the Visa first, then the personal loan, then the LOC

Result: Sarah cleared her last debt in month 11. Total interest paid over the period was approximately $2,800 — a fraction of what a minimum-payment approach would have cost. She estimates that following the minimum payment path would have taken 15–18 years and cost over $15,000 in interest on the credit card alone.

Sample Monthly Budget for a 12-Month Debt Sprint in Canada

Below is a sample monthly budget for a single Canadian earning $3,400/month (after tax) who is serious about paying off debt fast. Your numbers will vary, but use this as a framework:

TABLE 2: Sample Monthly Debt-Repayment Budget (Single Person, $3,400 Take-Home)

Category | Regular Budget ($) | Debt-Sprint Budget ($) | Savings ($) |

Rent / Housing | $1,200 | $1,200 | $0 |

Groceries | $500 | $320 | $180 |

Transportation (transit/gas) | $200 | $160 | $40 |

Utilities + Phone | $200 | $140 | $60 |

Streaming / Subscriptions | $80 | $15 | $65 |

Eating Out / Coffee | $250 | $50 | $200 |

Personal Care / Misc. | $150 | $80 | $70 |

Emergency Fund (small buffer) | $100 | $50 | $50 |

EXTRA Debt Payment | $200 | $885 | -$685 |

Side Hustle Income Added | — | +$500 | +$500 |

TOTAL Monthly to Debt | $200 | $1,885 | +$1,685 |

In this scenario, Sarah-style, you’re directing approximately $1,885/month to debt. Over 12 months that’s $22,620 — enough to cover the principal and interest on a $20,000 debt at average Canadian interest rates.

Canadian-Specific Tips and Resources You Should Know

Use a Credit Counselling Service (It’s Free)

If you’re overwhelmed, non-profit credit counselling is available across Canada at no cost. Organizations like Credit Counselling Canada (creditcounsellingcanada.ca) and the Canadian Association of Credit Counselling Services (CACCS) offer free debt assessments and budgeting help. These are legitimate, government-recognized services — not the sketchy debt settlement companies you see advertised on late-night TV.

Consider a Consumer Proposal If Debt Is Unmanageable

If $20,000 is just part of a larger debt load and you genuinely cannot make the numbers work, a Consumer Proposal through a Licensed Insolvency Trustee (LIT) may be worth exploring. It’s a formal, legal arrangement that lets you settle debt for less than you owe without going bankrupt. This is a last resort — but it exists for a reason, and it’s a Canadian-specific tool worth knowing about. [Office of the Superintendent of Bankruptcy: canada.ca/en/financial-consumer-agency — https://ised-isde.canada.ca/site/office-superintendent-bankruptcy/en]

GST/HST Credit and Canada Carbon Rebate as Debt Weapons

Many Canadians overlook government benefit payments as debt repayment opportunities. If you’re eligible for the GST/HST credit or the Canada Carbon Rebate (formerly the Climate Action Incentive), those quarterly payments — anywhere from $120 to $600+ per year depending on province and family size — should go straight to your debt during your 12-month sprint.

Tax Refund Timing Strategy

The average Canadian tax refund is approximately $1,800. File your taxes as early as possible (NETFILE opens in mid-February) and apply every dollar of your refund directly to your highest-interest debt. This one move alone can cover 9–10% of your $20,000 target in a single day.

Staying Motivated When the 12-Month Sprint Gets Hard

Let’s be real: month 3 and month 7 are usually when people quit. The initial excitement fades, the sacrifices feel heavier, and something always comes up — a car repair, a dental bill, a family event that costs money.

Here’s what actually keeps people on track:

Track Your Progress Visually

Print a simple debt tracker — a bar you fill in as your balance drops. There’s powerful psychology in seeing your debt shrink. Subreddits like r/PersonalFinanceCanada are full of Canadians posting their debt payoff progress charts, and the community accountability helps enormously.

Celebrate Milestones (Cheaply)

When you hit $5,000 paid off, celebrate — but cheaply. Cook a nice dinner at home, take a day trip, rent a movie. The point is to acknowledge progress without undoing it.

Build a Small Emergency Fund First

Before you go all-in on debt, set aside $500–$1,000 as a mini emergency fund. Without it, one unexpected expense forces you onto a credit card, which is demoralizing and costly. Think of it as insurance for your debt repayment plan.

Find Your ‘Why’

Write down what becoming debt-free means to you. Is it buying a home? Less stress? Being able to help your kids? Quitting a job you hate? Pin it somewhere visible. When you’re tired, that “why” is what keeps you going.

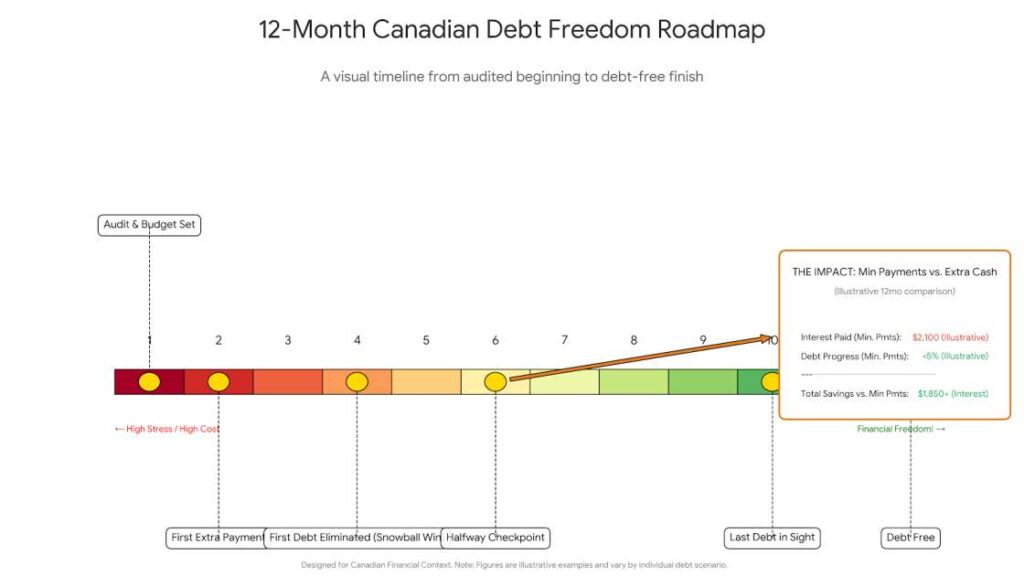

Conclusion: Your 12-Month Debt Freedom Plan Starts Today

Paying off $20,000 of debt in Canada in 12 months on an average income is not a get-rich-quick fantasy — it’s a math problem with a disciplined, structured solution. The Canadians who succeed aren’t the highest earners in the room. They’re the ones who got clear on the numbers, cut hard for a defined period, temporarily boosted their income, and stayed consistent through the discomfort.

To recap the key steps in your debt repayment plan:

- List every debt with balance, rate, and minimum payment

- Build a ruthless 12-month sprint budget

- Choose your strategy: avalanche, snowball, or hybrid

- Find ways to temporarily boost income by $400–$700/month

- Automate your payments so willpower isn’t required

- Negotiate lower rates and consider balance transfers

- Use Canadian tax tools (refund, benefit payments) as lump-sum weapons

- Track your progress visually and stay connected to your ‘why’

The average minimum-payment path on $20,000 at 19.99% could take over 30 years and cost more in interest than your original debt. The alternative — 12 focused months — changes everything that comes after.

You’ve got this. Start with Step 1 tonight.

DISCLAIMER

This article is for informational purposes only and does not constitute financial advice. For personalized guidance, consult a licensed financial advisor or non-profit credit counsellor. Statistics referenced are from publicly available Canadian government and industry sources as linked in the article.