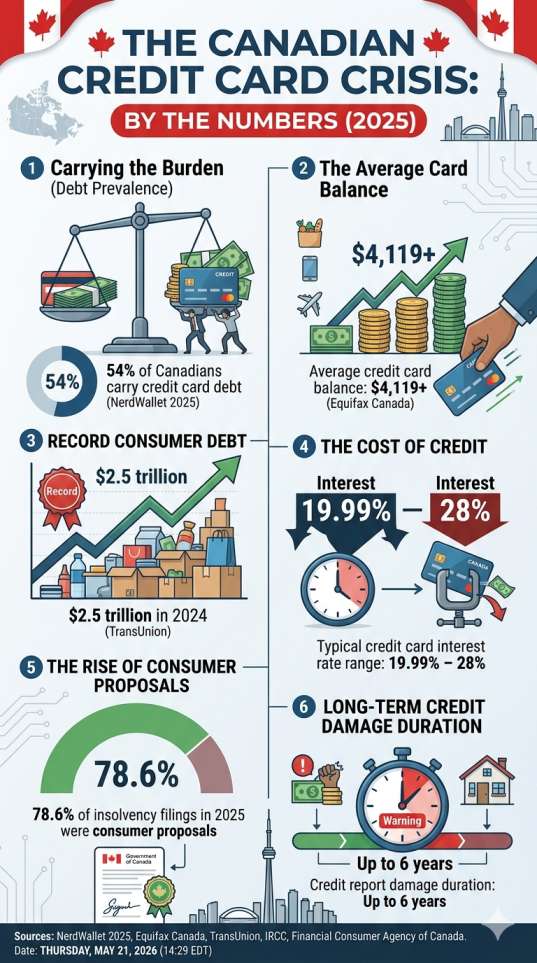

You’ve been juggling bills, the cost of groceries has gone through the roof, and one month — maybe two — you just can’t make that minimum credit card payment. You’re not alone. According to a 2025 NerdWallet Canada survey, 54% of Canadians currently carry credit card debt, and Canadian credit card debt hit a record $2.5 trillion in 2024, a staggering figure that reflects just how many households are stretched thin.

But here’s the thing: the moment you stop paying your credit card in Canada, a clock starts ticking. The consequences aren’t immediate catastrophe, but they do escalate — quickly, predictably, and sometimes permanently if left unaddressed.

This guide walks you through exactly what happens at each stage, what your legal rights are, what the credit card companies won’t tell you upfront, and — most importantly — what you can do about it.

The Timeline: What Happens Month by Month When You Miss Credit Card Payments

Understanding the timeline of consequences is the first step to managing the situation. The damage from missed payments follows a fairly predictable escalation, and knowing the stages lets you act before things spiral.

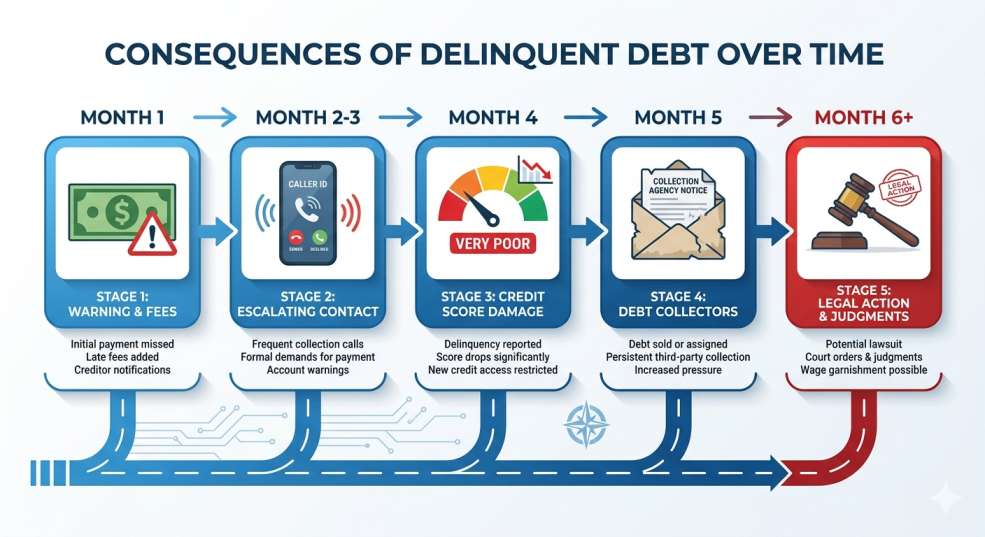

Month 1: The Late Fee and Interest Hit

The very first missed payment triggers an immediate late fee — typically $25 to $48 on most major Canadian cards. Your interest continues compounding daily on your outstanding balance. Most Canadian credit cards carry interest rates between 19.99% and 28%, which means on a $4,000 balance (the national average, per Equifax Canada), you could be accruing $65 or more in interest alone every single month.

You’ll likely receive a polite reminder letter or an automated email. Nothing on your credit report yet — but that window is short.

Month 2: Creditor Contact Begins

Two missed payments and the tone changes. Expect more persistent communication: phone calls, letters, and emails from your card issuer’s internal collections team. Your account may be flagged, and your credit limit could be frozen.

Still no collections agency involved, but the pressure is ramping up.

Month 3: Your Credit Report Takes the First Hit

This is where things get serious. After 30 days of non-payment, your delinquency is typically reported to Equifax Canada and TransUnion, Canada’s two major credit bureaus. A single missed payment appearing on your file can drop your credit score by 60 to 110 points depending on your starting score and overall credit profile.

At 90 days (three missed payments), many creditors will hand your file off to a collections agency. Your account status gets coded as “delinquent,” and the damage to your credit report deepens.

TABLE 1: Month-by-Month Consequences of Stopping Credit Card Payments in Canada

| Timeline | What Happens | Credit Impact |

|---|---|---|

| Month 1 | Late fee charged ($25–$48); interest compounds; reminder notice sent | None yet |

| Month 2 | Creditor calls and letters begin; account may be frozen | None yet (watch for 30-day mark) |

| Month 3 | 30+ day delinquency reported to Equifax & TransUnion; collections process begins | Score drops 60–110 points |

| Month 4–5 | Account sent to internal or third-party collections agency | Ongoing negative reporting |

| Month 6+ | Creditor may sell debt to collections agency; legal action risk rises | R9 rating possible; major score damage |

| Year 2–6 | Potential lawsuit, wage garnishment, asset liens | Negative mark stays up to 6 years |

What Happens to Your Credit Score — And for How Long?

Your credit score is one of the most lasting casualties of unpaid credit card debt. In Canada, negative information such as late payments, collections accounts, and defaults can remain on your credit report for up to six years from the date of first delinquency.

That’s six years of paying higher interest rates on car loans, being denied rental applications, and struggling to qualify for a mortgage — all because of payments you stopped making today.

Here’s how your credit rating code changes as your debt situation worsens:

- R1 – Pays on time. This is the goal.

- R7 – Making payments under a formal arrangement (e.g., consumer proposal)

- R9 – Bad debt; account written off; the lowest rating possible

Once your account hits R9, you’re in the most serious category. Rebuilding from here takes intentional effort, typically 12 to 24 months of consistent on-time payments plus at least two re-established credit lines, according to financial counsellors.

Collections: Your Rights as a Canadian Consumer

When your debt is sold or transferred to a collections agency, many Canadians panic — but you have more protection than you might think. Collection agencies in Canada are regulated provincially, and they must follow strict rules:

- They cannot contact you before 7 a.m. or after 9 p.m.

- They cannot use threatening, profane, or intimidating language.

- They cannot contact your employer except to confirm employment or garnish wages under a court order.

- They must identify themselves and the creditor they represent.

If a collections agency violates these rules, you can file a complaint with your provincial consumer protection office. Knowing your rights is the first line of defense against high-pressure tactics.

That said, ignoring collections entirely is not a strategy. If you stop making payments and ignore the agency, they can sue you for the money owed — and if the court rules in their favour, you could face wage garnishment or a lien on your property.

Legal Action: When Can They Actually Sue You?

This is the question most people are afraid to ask. Yes, your creditor or a collections agency can take you to court. If a money judgment is issued against you, the court can authorize:

- Wage garnishment – a portion of your paycheque goes directly to your creditor

- Bank account seizure – funds withdrawn directly from your accounts

- Property liens – a legal claim placed against real estate you own

The good news: there is a statute of limitations on how long they have to sue. In Canada, this varies by province — from two years (Ontario, British Columbia, Alberta) up to six years in others. At the time of writing, six years is the maximum statute of limitations in Canada, though this can reset if you make a payment or acknowledge the debt in writing.

Important: Don’t assume that a debt beyond the limitation period is gone. Creditors can still attempt to collect — they just lose the right to sue. Always consult a Licensed Insolvency Trustee (LIT) or legal professional before making decisions based on limitation periods.

What Are Your Real Options? A Practical Breakdown

The moment you realize you can’t keep up with your credit card payments, you have more choices than you think. Here they are, from least to most impactful on your credit, so you can match the solution to your situation.

Option 1: Contact Your Creditor Directly

This is always the first step, and it’s one most people skip out of embarrassment. Call your card issuer and explain your situation honestly. Many will offer:

- A temporary payment deferral

- A reduced interest rate for a hardship period

- A modified repayment schedule

Creditors would rather get something than nothing. This won’t appear on your credit report as a formal arrangement and has the least impact of all options.

Option 2: Debt Consolidation Loan

If you have a credit score in the mid-600s or above, a debt consolidation loan can roll multiple credit card balances into one monthly payment at a lower interest rate. This doesn’t reduce what you owe, but it makes repayment more manageable and stops the compounding chaos of multiple high-interest balances.

Word of caution: Once your credit cards are paid off through consolidation, resist the urge to use them again. Many Canadians fall into this exact trap and end up owing twice as much.

Option 3: Debt Management Plan (Credit Counselling)

A non-profit credit counselling agency can negotiate with your creditors on your behalf, combining your debts into a single monthly payment — often at reduced or eliminated interest. This won’t hurt your credit score the way a formal insolvency filing does, and it gives you professional support through the process.

Option 4: Consumer Proposal

A consumer proposal is a legally binding agreement filed through a Licensed Insolvency Trustee (LIT). You offer to repay a portion of what you owe — typically 20 to 50 cents on the dollar — over up to five years, with interest completely stopped. Once creditors accept (which happens in most cases), all collection calls, wage garnishments, and lawsuits stop immediately.

This option is available if you have between $1,000 and $250,000 in unsecured debt and a stable income to make regular payments. It appears on your credit report as an R7 rating, which is removed three years after completion or six years after filing — whichever comes first.

Notably, 78.6% of all consumer insolvency filings in Canada in the 12 months ending September 2025 were consumer proposals rather than bankruptcies — meaning most Canadians in serious debt are choosing this option.

Option 5: Bankruptcy

Bankruptcy is the last resort — and it’s not as catastrophic as many believe if your situation is truly unmanageable. Under bankruptcy, most unsecured debts (including credit cards) are discharged. A first-time bankruptcy typically takes 9 to 21 months depending on your income. It appears on your credit report for six to seven years after discharge, depending on the province, and you receive the lowest possible credit rating (R9).

Importantly, for many people already dealing with missed payments and collections, their credit is already severely damaged. Filing for formal relief — whether a proposal or bankruptcy — stops the bleeding and gives you a defined path forward.

TABLE 2: Comparing Your Debt Relief Options in Canada

| Option | Reduces Debt? | Credit Impact | Collections Stop? | Time to Complete | Best For |

|---|---|---|---|---|---|

| Call Your Creditor | Possibly (fees waived) | Minimal | No | Immediate | 1–2 missed payments |

| Debt Consolidation Loan | No (restructures it) | Minimal if on-time | No | Varies (1–7 yrs) | Good credit, manageable debt |

| Debt Management Plan | Partially (interest reduced) | Moderate | Yes (informal) | 3–5 years | Steady income, $10K–$50K debt |

| Consumer Proposal | Yes (up to 80% forgiven) | R7 (moderate) | Yes (legal stay) | Up to 5 years | $10K–$250K unsecured debt |

| Bankruptcy | Yes (most debts erased) | R9 (most severe) | Yes (legal stay) | 9–21 months | Unable to repay any amount |

A Real-World Scenario: What $8,000 in Credit Card Debt Can Cost You

Let’s make this concrete. Say you have an $8,000 credit card balance at 19.99% interest, and you stop paying entirely.

- Month 1: $130+ in interest, plus a $40 late fee = $170 added to your balance

- Month 3: Your balance is now approximately $8,500+, a collections notation appears on your credit file, and your score has dropped 80 points

- Month 6: The debt has been sold to a collections agency. They add their own fees. You’re now looking at $9,200+ owing, and a lawsuit is plausible.

- Year 2: A wage garnishment order means your employer withholds 20–30% of your take-home pay until the judgment is satisfied.

- Year 6: The negative mark finally drops from your credit report — if you took no action and simply waited it out.

Contrast that with a consumer proposal filed at Month 4: you might repay $3,500 over 3 years, interest stops, no wage garnishment, and your credit report clears three years after the proposal is paid off. The math is compelling.

How to Rebuild Your Credit After Missing Payments

Whether you’ve missed one payment or gone through a full consumer proposal, credit rebuilding follows the same fundamental steps.

Start with a secured credit card. These require a cash deposit equal to your credit limit, but they report to both Equifax and TransUnion, helping you build positive payment history immediately. Use it for one small recurring bill — a streaming subscription, for example — and set up autopay in full each month.

Keep your credit utilization below 30%. Ideally, aim for 10–20%. This single factor is one of the most powerful levers in your credit score calculation.

Never miss another payment. Payment history accounts for approximately 35% of your credit score. Consistency matters more than anything else.

Add a credit-builder loan. Some credit unions and online lenders offer small loans specifically designed for credit rebuilding. The payments get reported to the bureaus, building your profile without requiring strong existing credit.

Most people with a consumer proposal or bankruptcy on file can begin qualifying for better credit products within 12 to 24 months of consistent, responsible behaviour.

The Emotional Side Nobody Talks About

Let’s be honest — financial stress isn’t just a spreadsheet problem. A 2024 Bank of Canada analysis found that carrying a credit card balance significantly increases the likelihood of missing future debt payments, creating a self-reinforcing cycle that’s as psychological as it is financial.

If you’re avoiding opening bills, feeling shame about your debt, or losing sleep over collection calls — those feelings are valid. But avoidance makes everything worse. The single most valuable thing you can do is take one small action today: call your creditor, book a free appointment with a Licensed Insolvency Trustee, or reach out to a non-profit credit counsellor.

A free, confidential consultation with a Licensed Insolvency Trustee costs you nothing and gives you a clear picture of all your options under Canadian law. They are regulated professionals who are legally required to act in your best interest.

Key Takeaways

- Stopping credit card payments in Canada triggers a fast-moving escalation: late fees, credit score damage, collections, and potential legal action.

- Negative marks stay on your Canadian credit report for up to six years.

- You have legal protections against abusive collection practices — know your rights.

- Your options range from calling your creditor directly to a consumer proposal to bankruptcy — and each has a different cost, timeline, and credit impact.

- A consumer proposal stops interest and collections immediately and may allow you to repay as little as 20–50% of what you owe.

- Credit rebuilding after financial hardship is absolutely possible — typically within 12–24 months of responsible behaviour.

- The worst thing you can do is nothing. Action always beats avoidance.

Conclusion: You Have More Options Than You Think

If you’ve stopped paying your credit card — or you’re about to — the situation is serious but it is not hopeless. Millions of Canadians have been in exactly the same position and have rebuilt their financial lives completely.

The key is understanding the timeline, knowing your rights, and taking action before the consequences compound. Whether that action is a phone call to your bank this afternoon or a free consultation with a Licensed Insolvency Trustee this week, every step forward beats standing still.

Your credit score is not your worth. Your debt does not define your future. And in Canada, you have more legal tools and support resources available than most people realize.

Useful Resources

- Financial Consumer Agency of Canada – Credit Reports

- Office of the Superintendent of Bankruptcy Canada – Find a Licensed Insolvency Trustee

- Credit Canada – Free Credit Counselling

- BDO Debt Solutions – Statute of Limitations on Debt in Canada

- Equifax Canada – Check Your Credit Report

- TransUnion Canada – Check Your Credit Report

Disclaimer

The information in this article is intended for general educational and informational purposes only and does not constitute legal, financial, or professional advice. Laws, regulations, and credit bureau policies may vary by province and can change over time. Every financial situation is unique. Readers are strongly encouraged to consult with a Licensed Insolvency Trustee (LIT), a certified credit counsellor, or a qualified legal professional before making any decisions regarding their debt or financial situation. FrugalLiving.ca is not responsible for any actions taken based on the information provided in this article.