If you’ve been wondering when that quarterly tax-free payment from the government is landing in your account—and more importantly, how much you’re getting—you’re not alone. The GST/HST credit has become a financial lifeline for millions of Canadian households, and in 2026, it’s getting even bigger.

Here’s something that might surprise you: over 12 million Canadians are now eligible to receive this benefit, and many don’t even realize they qualify. With the recent transformation into the Canada Groceries and Essentials Benefit, payment amounts are increasing by 25% for five years, plus there’s a one-time top-up worth 50% of your annual credit coming this spring.

Whether you’re a single parent budgeting for groceries, a senior on a fixed income, or a young adult just starting out, understanding this benefit could put hundreds—even close to $2,000—back into your household budget this year.

What Is the GST/HST Credit? (And Why It Matters More Than Ever)

The GST/HST credit isn’t just another government payment—it’s specifically designed to help offset the goods and services tax (GST) or harmonized sales tax (HST) that you pay on everyday purchases throughout the year. Think of it as the government recognizing that sales tax hits lower-income households harder, proportionally, than wealthier ones.

In February 2026, the federal government officially transformed this program into the Canada Groceries and Essentials Benefit through Bill C-19, which received Royal Assent on February 12, 2026. The name change reflects a crucial reality: Canadians aren’t just dealing with regular inflation anymore—food prices have increased 27% in just five years, and the average family of four now spends $17,571.79 annually on groceries alone.

The Big Changes Coming in 2026

Here’s what makes 2026 different from previous years:

- One-time top-up payment: Equal to 50% of your 2025-26 annual credit, arriving by June 2026

- 25% permanent increase: Starting July 2026, your quarterly payments will be 25% higher for the next five years

- 500,000 new recipients: Income thresholds have been adjusted, making more Canadians eligible

According to the Department of Finance Canada, these changes will deliver $11.7 billion in support ($3.1 billion from the top-up and $8.6 billion from the ongoing increase).

2026 GST/HST Credit Payment Dates: Mark Your Calendar

The GST/HST credit operates on a quarterly schedule, meaning you receive payments four times per year. For 2026, here are the confirmed dates:

[TABLE 1: 2026 GST/HST Payment Schedule]

| Payment Date | Benefit Year | Special Notes |

|---|---|---|

| January 5, 2026 | 2025-26 | Already issued; standard quarterly amount |

| April 2, 2026 | 2025-26 | Includes the one-time 50% top-up |

| July 3, 2026 | 2026-27 | First payment with 25% increase |

| October 5, 2026 | 2026-27 | Increased quarterly amount continues |

Important timing note: If a payment date falls on a weekend or statutory holiday, the CRA deposits funds on the last business day before that date. Recipients enrolled in direct deposit receive funds on the exact payment date, while those receiving cheques should expect a 3-5 business day delay for mail delivery.

The April 2026 Payment: What Makes It Special

The April 2, 2026 payment deserves special attention because it includes the one-time top-up. If you received a GST/HST credit payment in January 2026, you’ll automatically receive this enhanced April payment without any additional application. According to Canada.ca, this top-up equals 50% of your entire 2025-26 annual entitlement, paid as a lump sum.

How Much Will You Actually Receive? The Complete Breakdown

The amount you receive depends on three key factors: your adjusted family net income (AFNI), your marital status, and the number of eligible children in your household. Let’s break down exactly what different households can expect.

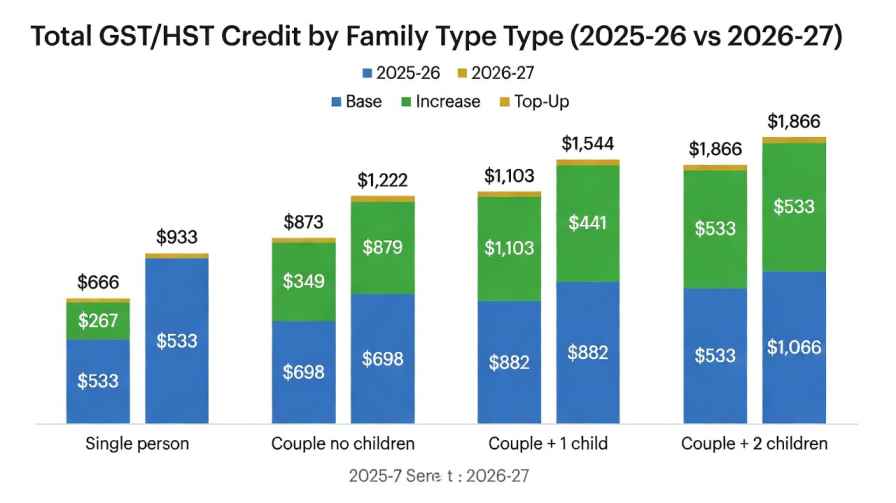

2025-26 Benefit Year (January & April 2026 Payments)

For the current benefit year, maximum annual amounts are:

[TABLE 2: Maximum Annual GST/HST Credit Amounts (2025-26)]

| Household Type | Maximum Annual Amount | Quarterly Payment | April 2026 Top-Up |

|---|---|---|---|

| Single individual | $533 | $133.25 | $267 |

| Married/Common-law couple | $698 | $174.50 | $349 |

| Each child under 19 | +$184 | +$46 | +$92 |

Real-world example: A couple with two children earning $40,000 combined would receive:

- Base couple amount: $698

- Two children: $184 × 2 = $368

- Total annual: $1,066

- Each quarter (Jan, July, Oct): $266.50

- April 2026 top-up: $533

- Total for April: $799.50

2026-27 Benefit Year (July & October 2026 Onwards)

With the 25% increase starting in July 2026, maximum annual amounts rise to approximately:

[TABLE 3: Projected Maximum Amounts with 25% Increase (2026-27)]

| Household Type | New Maximum Annual | Quarterly Payment | Increase from Previous Year |

|---|---|---|---|

| Single individual | $666 | $166.50 | +$133 annually |

| Married/Common-law couple | $873 | $218.25 | +$175 annually |

| Each child under 19 | +$230 | +$57.50 | +$46 annually |

What Families of Four Can Expect

Let’s look at the most common scenario—a family of four (two adults, two children):

Complete 2026-27 benefit year calculation:

- Base couple amount: $873

- Two children: $230 × 2 = $460

- Total for year: $1,333

- Plus April top-up: $533

- Grand total for 2026-27: $1,866

This aligns with government projections stating families of four could receive up to $1,890 when factoring in the one-time payment.

Who Qualifies for the GST/HST Credit? Complete Eligibility Rules

Understanding eligibility is crucial because many Canadians leave money on the table simply because they assume they don’t qualify. Let’s clear up the confusion.

Basic Eligibility Requirements

To receive the GST/HST credit, you must meet ALL of these criteria:

- Age requirement: You must be at least 19 years old before the month the payment is issued

- Exception: Those under 19 can qualify if they have (or had) a spouse/common-law partner, OR if they are (or were) a parent living with their child

- Residency requirement: You must be a Canadian resident for income tax purposes during:

- The month before the payment

- At the beginning of the payment month

- Tax filing requirement: You MUST file your income tax return annually, even if you have zero income to report

The third requirement trips up many people. According to the Canada Revenue Agency, failure to file your tax return is the single most common reason eligible Canadians miss out on this benefit.

Income Thresholds: Will You Receive the Full Amount?

The GST/HST credit is income-tested, meaning payments gradually decrease as your adjusted family net income (AFNI) rises above certain thresholds. Here’s how it works:

[TABLE 4: Income Phase-Out Thresholds (2024 Tax Year)]

| Household Type | Reduced Credit Starts | No Longer Entitled |

|---|---|---|

| Single, no children | $45,000 | $56,181 |

| Married/Common-law, no children | $45,000 | $60,000+ |

| Single parent, 1 child | $45,000 | $65,000+ |

| Couple with 2 children | $45,000 | $74,201 |

How phase-out works: Once your AFNI exceeds the base threshold of approximately $45,000, your credit is reduced by 5% of the amount over the threshold until it reaches zero.

Phase-out example: Sarah is single with an AFNI of $50,000 (no children).

- Maximum credit she could receive: $533

- Income above threshold: $50,000 – $45,000 = $5,000

- Reduction: $5,000 × 5% = $250

- Actual credit: $533 – $250 = $283 annually ($70.75 per quarter)

What Counts as “Adjusted Family Net Income”?

Your AFNI is calculated from Line 23600 of your tax return, with some adjustments:

Includes:

- Employment income

- Self-employment income

- Investment income

- Taxable pensions and retirement income

- Employment Insurance benefits

- Registered Disability Savings Plan (RDSP) income

- Universal Child Care Benefit (UCCB) income (if applicable)

Does NOT include:

- GST/HST credit payments themselves

- Canada Child Benefit payments

- Most social assistance payments

- Workers’ compensation

- War veterans’ allowances

Special Eligibility Situations: Answers to Unique Circumstances

Students and Young Adults

Many 19-year-olds and students wonder if they qualify. Here’s the truth: Yes, most students are eligible if they file a tax return, even with minimal or zero income. Your eligibility is based on your personal AFNI, not your parents’ income, once you turn 19.

Student scenario: Jordan, 20, is a full-time university student earning $8,000 annually from a part-time job. Their parents claim education expenses on their own returns, but Jordan files independently. Jordan qualifies for the full $533 annual credit because their income is well below the threshold.

Seniors and Retirees

Seniors often have the most to gain from this credit, especially those on fixed incomes. If you receive Old Age Security (OAS) or the Guaranteed Income Supplement (GIS), you likely qualify for the GST/HST credit as well—and these benefits don’t affect each other.

According to government examples, a single senior with $25,000 in net income would receive:

- Regular 2026-27 credit: $666

- April top-up: $267

- Total for year: $933

This represents an increase of $402 compared to the previous year—a meaningful boost for those managing tight budgets.

Newcomers to Canada

If you’ve recently become a Canadian resident, you won’t be automatically assessed for the GST/HST credit until you file your first tax return. However, you can apply before filing using:

- Form RC151 (GST/HST Credit Application for Individuals Who Become Residents of Canada) – if you don’t have children

- Form RC66 (Canada Child Benefits Application) – if you have children under 19

New residents should submit their application to their local CRA tax centre along with proof of birth for any children and proof of Canadian residency status.

Shared Custody Parents

If you share custody of a child with another parent, both of you may be eligible for half of the GST/HST credit amount for that child. This typically applies when:

- Both parents receive the Canada Child Benefit (CCB) for the same child on a shared basis

- You have a legal custody arrangement confirming shared parenting

The CRA determines shared custody eligibility based on your CCB status. If you already receive shared CCB payments, your GST/HST credit should reflect this automatically.

How to Apply for the GST/HST Credit (Or Why You Don’t Need To)

Here’s the best news: for most Canadians, there is no application process. The CRA automatically assesses your eligibility when you file your annual income tax return.

The Automatic Assessment Process

When you file your tax return (by the April 30 deadline each year), the CRA:

- Reviews your reported income and family situation

- Calculates your AFNI

- Determines if you’re eligible and how much you’ll receive

- Updates your benefit entitlement for the July-to-June benefit year

- Issues payments automatically via your chosen method (direct deposit or cheque)

You’ll receive a Notice of Determination letter confirming your GST/HST credit entitlement after your tax return is assessed. This letter shows:

- Your annual credit amount

- Your quarterly payment schedule

- The benefit year it covers

- Any related provincial or territorial credits

What Happens If You File Late?

Filing after the April 30 deadline can temporarily disrupt your GST/HST credit payments. Here’s what typically happens:

Scenario: Maria normally files in March but this year doesn’t file until August.

- January & April 2026 payments: She receives these on schedule because they’re based on her 2024 tax return (already on file)

- July 2026 payment: This payment is delayed because it starts a new benefit year based on her 2025 return—which she hasn’t filed yet

- Once she files in August: The CRA processes her return and issues any missed payments as a retroactive lump sum in her next scheduled payment (October)

Bottom line: File on time (by April 30) to avoid payment disruptions, even if you owe no taxes or have no income to report.

Keeping Your Information Current

Your GST/HST credit can be affected by life changes. You should update your CRA account within one month if:

- You get married or enter a common-law partnership

- You separate or divorce

- Your spouse or common-law partner passes away

- You have a child or welcome a child into your care

- A child leaves your care

- You change your address

- You change your direct deposit information

Update your information through CRA My Account or by calling 1-800-387-1193.

Enable direct deposit through CRA My Account to receive payments faster and more securely. Direct deposits arrive on the exact payment date, while cheques can take up to 10 business days to arrive by mail.

PRO TIP

Provincial and Territorial Credits: You Might Be Getting More Than You Think

Many Canadians don’t realize that the payment they receive labeled “GST/HST Credit” often includes provincial or territorial benefits delivered through the same system. These additional amounts are automatically calculated and added to your federal credit—no separate application needed.

Additional Credits by Province/Territory

[TABLE 5: Provincial and Territorial Credits Delivered with GST/HST]

| Province/Territory | Additional Credit Name | Who Administers It |

|---|---|---|

| Ontario | Ontario Sales Tax Credit, Ontario Energy and Property Tax Credit (OEPTC) | Province via CRA |

| Alberta | Alberta Child and Family Benefit (ACFB) | Province via CRA |

| British Columbia | BC Climate Action Tax Credit | Province via CRA |

| Saskatchewan | Saskatchewan Low-Income Tax Credit | Province via CRA |

| Manitoba | None delivered with GST/HST | N/A |

| Nunavut | Nunavut Cost of Living Offset | Territory via CRA |

| Northwest Territories | NWT Cost of Living Offset | Territory via CRA |

| Yukon | None delivered with GST/HST | N/A |

Filing your annual tax return ensures you’re considered for all applicable federal, provincial, and territorial benefits. In some provinces like Ontario, eligible households can receive several hundred additional dollars annually through these combined credits.

Common Questions and Troubleshooting

“I Haven’t Received My Payment—What Should I Do?”

If your expected payment date has passed and you haven’t received your deposit or cheque:

Step 1: Check your CRA My Account (usually available 10 days after the payment date)

- Log in at canada.ca/my-cra-account

- Navigate to “Benefits and Credits”

- View your GST/HST credit status and payment history

Step 2: Verify your eligibility

- Confirm you filed your most recent tax return

- Check that your income doesn’t exceed the phase-out threshold

- Ensure your marital status and address are current

Step 3: Common reasons for delays or stopped payments

- Recently turned 19: Your first payment won’t arrive until the next payment date after your birthday

- Change in marital status: If you got married or separated, it can take 1-2 payment cycles to reflect the change

- Low annual amount: If your total annual credit is less than $50, the CRA pays it as a single lump sum in July instead of quarterly

- Outstanding CRA debts: In some cases, credits can be applied to tax debts or benefit overpayments

- Address issues: If receiving by cheque and you’ve moved, the cheque may be returned

Step 4: Contact the CRA If you’ve verified everything above and still haven’t received payment:

- Call the CRA Benefits Enquiries line: 1-800-387-1193

- Have your Social Insurance Number and date of birth ready

- Hold times can be long; call early in the morning or late in the afternoon for shorter waits

“Can I Receive the Credit If I Have No Income?”

Yes, absolutely. The GST/HST credit is specifically designed to help low-income Canadians, including those with zero income. You still must file a tax return to be assessed, but you’ll likely receive the maximum credit amount if you have no income reported.

Zero-income scenario: Ahmed is between jobs and earned $0 in 2024. He files his 2024 tax return anyway (reporting zero income), and because his AFNI is $0, he qualifies for the full maximum credit as a single individual: $533 annually, or $133.25 per quarter.

“I’m on Social Assistance—Can I Still Get the Credit?”

Yes. Provincial social assistance payments are generally not considered income for GST/HST credit purposes. Many people receiving social assistance also receive the maximum GST/HST credit because their taxable income is at or near zero.

However, some provinces may adjust your social assistance payments if you receive additional income from tax credits. Check with your province’s social services department for specific rules.

“What If My Income Increased This Year?”

Your GST/HST credit for the July 2026 to June 2027 benefit year is based on your 2025 tax return (which you’ll file in spring 2026). If your income increases significantly from 2024 to 2025, your credit may be reduced or eliminated starting with the July 2026 payment.

The April 2026 top-up payment is based on your January 2026 eligibility, which uses your 2024 tax information—so an income increase in 2025 won’t affect that specific payment.

Maximizing Your GST/HST Credit: Strategic Tips

While you can’t control the credit amount you’re entitled to (it’s based on your income), you can ensure you receive every dollar available to you.

1. File Your Tax Return Every Single Year

This cannot be emphasized enough. Even in years where you earn little or nothing, filing ensures:

- Continuous GST/HST credit payments

- Eligibility for the Canada Child Benefit (if you have children)

- Consideration for provincial and territorial credits

- No retroactive payment complications

The CRA can only recalculate and issue retroactive GST/HST credits for the current year and three previous years. If you haven’t filed in several years, you could be missing thousands of dollars in benefits.

2. Register for Direct Deposit Immediately

Direct deposit is faster, more secure, and eliminates the risk of lost or stolen cheques. Set it up through:

- CRA My Account online

- Your online banking portal (many banks offer CRA direct deposit enrollment)

- By calling the CRA at 1-800-959-8281

3. Update Life Changes Promptly

Major life events can increase your GST/HST credit entitlement:

- Having a child: Adds $184 annually ($230 starting July 2026)

- Separation or divorce: May increase your individual credit if you now qualify as single

- Becoming a sole-support parent: Increases your credit substantially

Update changes through CRA My Account within one month of the event.

4. Consider Income Splitting Strategies (Legally)

If you’re married or in a common-law relationship, legitimate income splitting can potentially keep your combined AFNI below phase-out thresholds:

- Spousal RRSP contributions: Higher-earning spouse contributes to lower-earning spouse’s RRSP, reducing household AFNI when withdrawn in retirement

- Pension income splitting: Retirees can split up to 50% of eligible pension income between spouses

- TFSA for investment income: Tax-Free Savings Account growth doesn’t count toward AFNI

Always work with a qualified tax professional before implementing income splitting strategies. The CRA has strict rules about income attribution, and improper splitting can result in penalties.

CAUTION

5. Check Your Notice of Assessment Carefully

After filing your tax return, review your Notice of Assessment to verify:

- Your reported income matches what you filed

- Your marital status is correct

- The number of children in your care is accurate

- Your GST/HST credit calculation seems reasonable

Errors on your Notice of Assessment can be corrected by calling the CRA or filing an adjustment request through CRA My Account.

The Bigger Picture: Why the GST/HST Credit Matters for Canadian Households

Beyond the mechanics of payment dates and calculations, the GST/HST credit represents an important piece of Canada’s social safety net—and its expansion in 2026 comes at a critical time.

The Food Affordability Crisis

According to Canada’s Food Price Report 2026, grocery prices have increased 27% over just five years. Last December, Canada recorded food inflation of 6.2% year-over-year—nearly double the U.S. rate and triple the rate in Germany and France.

For perspective: The average Canadian family of four now spends $17,571.79 annually on food, an increase of almost $1,000 from 2025 alone.

Dr. Sylvain Charlebois, Director of the Agri-Food Analytics Lab at Dalhousie University, notes that while the GST/HST credit increase will help offset short-term inflation, “Canada’s food affordability crisis is structural and requires deeper reforms” beyond benefit payments.

The Impact on Low-Income Households

Research consistently shows that sales taxes are regressive—meaning they consume a larger percentage of income for lower-income households. A family earning $30,000 annually spends virtually all of it on taxable goods and services (housing, food, transportation, clothing), while a family earning $150,000 can save or invest a significant portion.

The GST/HST credit partially corrects this imbalance by returning tax revenue to those who need it most. For many recipients, the quarterly payments:

- Help cover utility bills during expensive winter months

- Provide a buffer for unexpected expenses

- Allow purchase of essentials that might otherwise be delayed

- Reduce reliance on high-interest debt or payday loans

Economic Stimulus Effect

Government benefits like the GST/HST credit also serve as automatic economic stabilizers. When 12 million Canadians receive an extra $3.1 billion in purchasing power (from the 2026 top-up alone), that money flows directly into the economy—at grocery stores, for rent payments, toward utility bills, and for other essential expenses.

Unlike tax cuts that disproportionately benefit higher earners who may save the difference, benefit payments to low and modest-income households have a high “marginal propensity to consume”—economic jargon meaning the money gets spent rather than saved, stimulating economic activity.

Looking Ahead: What to Expect Beyond 2026

The transformation into the Canada Groceries and Essentials Benefit isn’t just a rebrand—it signals a longer-term commitment to supporting Canadian households facing affordability challenges.

The Five-Year Commitment (2026-2031)

The 25% increase to the benefit will remain in place through the 2030-31 benefit year, providing predictable support for households planning their finances over the medium term. According to Parliamentary Budget Officer estimates, this commitment will deliver $8.6 billion in additional support over that period.

Potential Future Adjustments

While the 25% increase is locked in, the credit amounts continue to be indexed to inflation annually, meaning:

- In years with higher inflation, your credit will increase accordingly

- If inflation moderates, increases will be smaller but still present

- The “real” purchasing power of the credit should remain relatively stable

This indexation has historically been based on the Consumer Price Index (CPI), which the Bank of Canada targets at 2% annually (though actual inflation has been higher in recent years).

The Broader Affordability Strategy

The Canada Groceries and Essentials Benefit is part of a larger government strategy to address cost-of-living challenges, which also includes:

- National School Food Program: Providing school meals for up to 400,000 children annually, potentially saving participating families with two children approximately $800 per year

- Automatic Federal Benefits: Starting with the 2026 tax year, ensuring up to 5.5 million low-income Canadians automatically receive benefits they qualify for

- Strategic Response Fund: $500 million to help businesses address supply chain disruptions without passing costs to consumers

- Food Security Fund: $150 million under the Regional Tariff Response Initiative for small and medium enterprises

Whether these broader initiatives successfully address Canada’s structural food affordability challenges remains to be seen, but the GST/HST credit expansion provides immediate, tangible relief to millions of households right now.

Taking Action: Your Next Steps

Understanding the GST/HST credit is valuable, but taking action ensures you actually receive the money you’re entitled to. Here’s exactly what to do based on your situation:

If you’ve already filed your 2024 tax return:

✓ You’re all set for payments through June 2026 ✓ Mark April 2, 2026 on your calendar for the top-up payment ✓ File your 2025 return by April 30, 2026 to receive the increased July 2026 payment ✓ Set up or verify your direct deposit information at canada.ca/my-cra-account

If you haven’t filed your 2024 tax return yet:

- Gather your 2024 tax slips (T4, T5, etc.)

- File as soon as possible—even if you have no income to report

- You may still receive retroactive payments once processed

- Consider using free tax clinics if you need assistance (find them at canada.ca/taxes-help)

If you’re new to Canada:

- File your first tax return to be automatically assessed for future years

- Complete Form RC151 (no children) or RC66 (with children) for immediate consideration

- Submit to your local CRA tax centre with proof of residency and children’s birth certificates

- Expect processing to take 8-12 weeks for manual applications

If you think you should be receiving more:

- Log into CRA My Account and review your “Benefits and Credits” section

- Verify your marital status, number of children, and address are correct

- Check your most recent Notice of Assessment for any discrepancies

- Call 1-800-387-1193 if you identify errors that need correction

Final Thoughts: Making the Most of This Financial Support

The GST/HST credit—now the Canada Groceries and Essentials Benefit—has evolved into one of the federal government’s most direct responses to affordability challenges facing millions of Canadian households. With the 2026 enhancements, a family of four could receive up to $1,890 this year, with continued elevated support through 2031.

But here’s what really matters: this money is already yours if you qualify—you just need to claim it by filing your taxes.

Every year, thousands of eligible Canadians miss out on GST/HST credits simply because they don’t file a tax return. Whether you’re a student with minimal income, a senior on a fixed pension, someone between jobs, or working and raising a family—if your income falls below the thresholds, you likely qualify.

The quarterly deposits might seem modest on their own, but over the course of a year, they add up to meaningful support for groceries, utilities, rent, and other essentials. And with food prices continuing to climb, every bit helps.

Take 30 minutes today to check your CRA My Account, verify your information is current, and if you haven’t already, file your 2024 tax return. Your future self—and your grocery budget—will thank you.

Key Takeaways

✓ GST/HST credit is now the Canada Groceries and Essentials Benefit with 25% higher payments starting July 2026

✓ Over 12 million Canadians qualify, including those with zero income who file tax returns

✓ April 2026 includes a special one-time top-up worth 50% of your annual credit

✓ Payments arrive quarterly on January 5, April 2, July 3, and October 5 in 2026

✓ Maximum amounts for 2026-27: Singles get $666/year, couples $873/year, plus $230 per child

✓ No separate application needed—just file your annual tax return by April 30

✓ Set up direct deposit for fastest, most secure payment delivery

✓ Update life changes (marriage, children, separation) within one month to adjust your credit

✓ Provincial and territorial credits may be included automatically with your federal payment

✓ File even with no income to ensure continuous eligibility and avoid retroactive complications