If you’ve ever wondered how your neighbour manages to take yearly vacations, drive a reliable car, and still have money in savings—all while earning a modest income—you’re not alone. The secret isn’t a six-figure salary or a large inheritance. It’s something far more accessible: living well below their means.

Canadians have quietly mastered the art of frugal living, not through deprivation, but through intentional choices that align spending with values. Unlike the restrictive penny-pinching portrayed on reality TV, true frugality is about maximizing value, minimizing waste, and creating financial breathing room for what truly matters.

In this comprehensive guide, we’re pulling back the curtain on 30 practical habits that help everyday Canadians build wealth, reduce financial stress, and achieve their goals—whether that’s early retirement, debt freedom, or simply sleeping better at night. These aren’t extreme measures or unrealistic expectations. They’re sustainable strategies you can implement starting today, regardless of your current income level.

Understanding Living Below Your Means: More Than Just Cutting Costs

What Does “Living Below Your Means” Really Mean?

Living below your means isn’t about extreme sacrifice or eating ramen noodles every night. It’s the practice of consistently spending less than you earn, creating a financial buffer that opens doors rather than closing them.

According to recent financial studies, the average Canadian household saves approximately 6-8% of their disposable income, but those who intentionally live below their means often save 15-25% or more. The difference? Mindset and method.

The Three Pillars of Living Below Your Means: 1. Awareness: Knowing exactly where your money goes each month 2. Intentionality: Making spending decisions that reflect your priorities 3. Consistency: Maintaining habits even when income increases

Why Canadians Excel at Frugal Living

Canadian culture naturally lends itself to frugal habits. The long winters encourage planning ahead, storing up, and making things last. Additionally, the higher cost of living in major cities like Toronto, Vancouver, and Montreal has forced many Canadians to develop creative solutions for stretching their dollars.

The Foundation: Money Management Essentials

1. Track Every Dollar (Yes, Every Single One)

The first rule of living below your means is knowing where your money actually goes. Most Canadians who successfully save are meticulous trackers, whether through apps, spreadsheets, or good old-fashioned paper ledgers.

Use free Canadian budgeting apps or a simple spreadsheet. Track for at least 30 days to identify spending patterns you didn’t know existed.

IMPLEMENTATION TIP

2. Build a Buffer Before You Need It

Successful frugal Canadians prioritize their emergency fund above almost everything else. Even setting aside $25-50 per paycheck creates a cushion that prevents debt when unexpected expenses arise.

The target? Three to six months of essential expenses. Start with $1,000 as your first milestone.

3. Pay Yourself First, Not Last

Waiting until the end of the month to save what’s “leftover” is a recipe for empty savings accounts. Instead, automate transfers to savings the same day your paycheck arrives. If you never see the money, you won’t spend it.

4. Master the 24-Hour Rule

Before making any non-essential purchase over $50, wait 24 hours. This simple pause eliminates impulse buying and gives you time to determine if it’s a genuine need or momentary want.

5. Create Sinking Funds for Irregular Expenses

Car insurance, property taxes, holiday gifts—these predictable irregular expenses derail budgets when treated as surprises. Frugal Canadians divide annual costs by 12 and set aside money monthly so funds are ready when bills arrive.

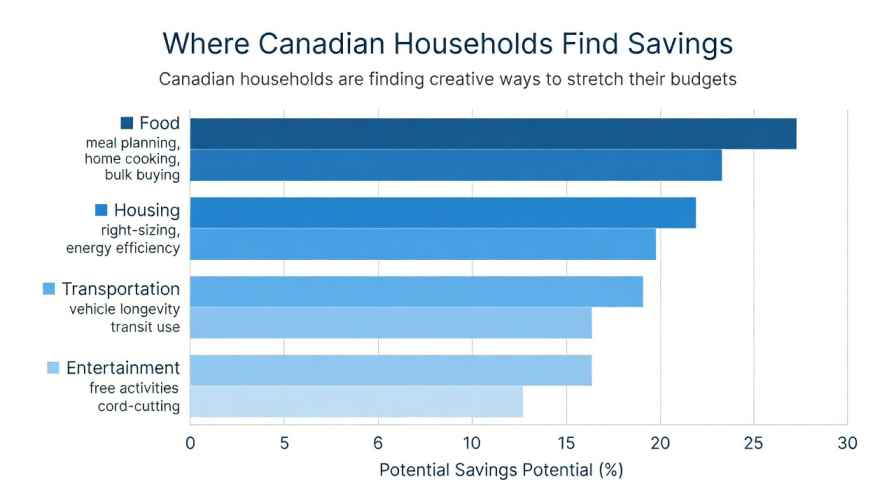

Housing: Your Biggest Opportunity for Savings

6. Right-Size Your Living Space

Housing typically consumes 30-40% of income. Successful frugal Canadians often choose smaller homes or apartments in less trendy neighbourhoods, banking the difference rather than maximizing their approved mortgage amount.

Real Example: A couple in Ottawa chose a 2-bedroom condo in Kanata over a 3-bedroom townhouse downtown, saving $800 monthly. Over five years, that’s $48,000 plus investment growth.

7. Negotiate Your Rent (Yes, It Works!)

Many Canadian renters don’t realize rent is negotiable, especially for good tenants willing to sign longer leases. One conversation could save you $50-100 monthly—$600-1,200 annually.

8. DIY Home Maintenance When Possible

YouTube has revolutionized home maintenance. Simple tasks like changing furnace filters, caulking windows, unclogging drains, or painting rooms cost pennies compared to hiring professionals.

Cost savings: $200-500 annually by handling 3-4 simple maintenance tasks yourself.

9. Optimize Your Home Temperature Settings

Adjusting your thermostat by just 3 degrees (down in winter, up in summer) when you’re away or sleeping can reduce heating and cooling costs by 5-15%. Programmable thermostats automate this process.

[TABLE 1: Annual Savings from Temperature Adjustments]

| Adjustment | Annual Savings (Average Canadian Home) | 10-Year Total |

|---|---|---|

| 2°C decrease in winter | $150-200 | $1,500-2,000 |

| 2°C increase in summer | $75-100 | $750-1,000 |

| Programmable thermostat | $180-250 | $1,800-2,500 |

| Combined strategies | $400-550 | $4,000-5,500 |

Source: Natural Resources Canada, 2024 estimates

10. Embrace the Capsule Wardrobe Concept

Instead of closets bursting with rarely-worn clothes, frugal Canadians build quality capsule wardrobes with versatile pieces that mix and match. This reduces spending while simplifying daily decisions.

Food: Smart Strategies for Your Second-Largest Expense

11. Meal Plan Like a Pro

Canadians who meal plan report saving $200-400 monthly on groceries. Planning prevents overbuying, reduces food waste, and eliminates expensive last-minute takeout decisions.

Pro tip: Plan meals around what’s on sale and in season, then shop with a specific list.

12. Cook in Bulk and Freeze Smartly

Batch cooking on weekends provides quick weeknight meals while maximizing ingredient use. Frugal Canadians often double recipes, freezing portions for busy weeks.

13. Shop Ethnic Markets for Fresh Produce

Asian, Middle Eastern, and Latin American grocery stores often offer fresh produce at 30-50% less than mainstream supermarkets, with better quality and selection.

14. Use Cashback Apps and Grocery Loyalty Programs

Apps like Checkout 51, Caddle, and Scene+ turn routine grocery shopping into earning opportunities. Combined with store loyalty programs, savvy shoppers earn $30-60 monthly.

[TABLE 2: Monthly Cashback Potential Comparison]

| Strategy | Time Investment | Monthly Return | Annual Total |

|---|---|---|---|

| Checkout 51 | 5 min/week | $15-25 | $180-300 |

| Scene+ Points | None (automatic) | $10-15 | $120-180 |

| Flipp App (flyer browsing) | 10 min/week | $20-40 | $240-480 |

| Combined approach | 20 min/week | $45-80 | $540-960 |

15. Master the Art of “Eating Down the Pantry”

Before your next shopping trip, challenge yourself to create meals from existing pantry and freezer items. This reduces waste and often yields surprising culinary creativity.

16. Brew Coffee at Home

Tim Hortons runs can cost $3-5 daily. At $4 per day, five days weekly, you’re spending $1,040 annually. A quality home setup costs $100-200 upfront, then pennies per cup.

Annual savings: $800-900 by brewing at home.

17. Shop Seasonal Produce and Freeze or Preserve

Berries in summer, squash in fall, root vegetables in winter—buying in season and preserving through freezing, canning, or pickling provides year-round access at peak prices.

Transportation: Moving Smart, Not Expensive

18. Extend Your Vehicle’s Lifespan

Frugal Canadians drive vehicles for 10-15 years, not 3-5. Regular maintenance costs far less than depreciation and car payments.

Financial impact: Keeping a paid-off car for three extra years instead of upgrading saves approximately $15,000-25,000.

19. Consider One-Car Households

In cities with decent transit, many couples successfully share one vehicle, saving insurance, maintenance, and depreciation costs.

Annual savings: $4,000-7,000 depending on the region.

20. Maximize Public Transportation and Cycling

Monthly transit passes in major Canadian cities cost $100-160, while owning and operating a vehicle costs $800-1,200 monthly. Even partial use generates significant savings.

21. Learn Basic Car Maintenance

Oil changes, tire rotations, air filter replacements, and battery checks can all be learned through YouTube tutorials, saving $300-600 annually in labour costs.

Entertainment and Lifestyle: Fun Without the Financial Hangover

22. Embrace Free Community Events

Canadian cities offer countless free festivals, concerts, museums (on specific days), outdoor movies, and community programs. Check municipal websites and library bulletin boards.

23. Maximize Library Privileges

Modern Canadian libraries offer far more than books—digital magazines, streaming services, video games, tool libraries, skill classes, and meeting spaces, all free with your library card.

24. Host Potluck Gatherings Instead of Restaurant Outings

Social connection doesn’t require expensive restaurant bills. Potluck dinners, game nights, and backyard barbecues provide fellowship at fraction of the cost.

25. Cut the Cord Strategically

Many frugal Canadians have eliminated cable TV ($80-150 monthly) in favour of one or two streaming services ($20-30 combined), saving $600-1,440 annually.

26. Time Major Purchases Around Sale Cycles

Black Friday, Boxing Day, end-of-season clearances—patient Canadians save 30-70% by timing purchases strategically rather than buying when the urge strikes.

The Mindset Shifts That Make It All Work

27. Define “Enough” for Your Life

The hedonic treadmill keeps people perpetually chasing more. Frugal Canadians define what “enough” looks like for their family, then protect that definition against lifestyle inflation.

28. Practice Contentment, Not Comparison

Social media showcases everyone’s highlight reel. Successful frugal living requires focusing on your own path and values rather than keeping up with others’ curated lives.

29. View Money as Life Energy

Every dollar represents time you traded from your life. This perspective shift transforms spending decisions—is this purchase worth X hours of my life?

30. Celebrate Progress, Not Perfection

Living below your means is a journey with setbacks and learning curves. Frugal Canadians celebrate small wins—an extra $50 saved, a no-spend weekend accomplished—rather than beating themselves up over mistakes.

The Compound Effect: What These Habits Really Create

Living below your means isn’t about one dramatic change—it’s the accumulation of dozens of small, consistent decisions. Let’s visualize the real financial impact.

Real Canadian Success Stories

Sarah from Halifax: By implementing just 10 of these habits, Sarah paid off $23,000 in consumer debt in 18 months while earning $45,000 annually. Her key strategies? Meal planning, selling her second car, and moving to a smaller apartment.

The Chens from Calgary: This family of four reduced monthly expenses by $800 by cutting cable, shopping at ethnic markets, and DIY home maintenance. They redirected savings to their children’s education fund, accumulating over $45,000 in five years.

Marcus from Winnipeg: Living solo on $52,000 yearly, Marcus achieved a 30% savings rate by embracing minimalism, cooking all meals, and biking year-round. He reached his house down payment goal in three years.

Common Challenges and How to Overcome Them

“But I’m Already Struggling to Make Ends Meet”

If you’re genuinely earning barely enough for essentials, focus on increasing income rather than further restriction. Side hustles, skill development, and career advancement may be more impactful than extreme frugality.

“My Partner Isn’t On Board”

Financial decisions work best when partners align. Start with small, non-threatening changes and share success stories. Focus on shared goals rather than restrictions.

“I Feel Deprived and Resentful”

This signals you’ve swung too far toward restriction. Effective frugality builds in intentional spending on what you value. Adjust your approach to feel sustainable, not punishing.

“My Income Just Increased—Can I Relax Now?”

This is where many people stumble. Instead, bank at least 50% of raises and bonuses. This accelerates financial goals while still allowing lifestyle improvements.

Action Steps: Your 30-Day Challenge

Ready to start living below your means? Here’s your month-one action plan:

Week 1: Track every expense without judgment. Just observe your patterns.

Week 2: Calculate your current savings rate. Choose 3 habits from this article to implement.

Week 3: Automate savings transfers. Create your first sinking fund.

Week 4: Evaluate progress. What worked? What felt too restrictive? Adjust accordingly.

Remember: sustainable change happens gradually. You’re not aiming for perfection in month one—you’re building awareness and momentum.

Conclusion: Freedom Through Intention

Living below your means isn’t about deprivation—it’s about liberation. Every habit in this guide represents a choice: to value long-term security over short-term gratification, to define success on your own terms rather than society’s expectations, and to create financial breathing room in an expensive world.

The Canadians who successfully live well below their means aren’t inherently more disciplined or blessed with higher incomes. They’ve simply chosen to be intentional about where their money goes, one decision at a time.

Will every habit resonate with your life? Absolutely not. But if even five of these 30 strategies find a place in your routine, you’ll see measurable progress within months. And that progress compounds—financially, emotionally, and in terms of the options available to you.

The journey to financial freedom doesn’t start with a windfall or a six-figure income. It starts with a single intentional choice. Which habit will you implement first?